Orange County’s economy will sour along with the nation as local home prices fall by 11% in the next six months, Chapman University economists forecast.

The school’s semiannual economic outlook, released Thursday, June 22, calls for mild national recession in the second half of the year.

“We’re even more confident that there will be a recession,” said Chapman economic professor Jim Doti, who predicted a late 2023 downturn in the school’s December forecast.

The culprit is no surprise: the Federal Reserve’s boosting of interest rates. Chapman’s downcast view sees the pricier financing throttling an overheated national economy that produced the worst bout of inflation in four decades, Those tight-money policies will sharply curtail hiring and real estate investments as 2023 winds down.

And Chapman isn’t alone. Cal State Fullerton economists predicted in April a mild, “garden-variety” recession that will stall the local economy for the rest of 2023 and through 2024..

Local letdown

Look at the oncoming recession’s Orange County impact as detailed by Chapman’s projections …

The 1.7 million jobs countywide at year’s end will be off 1% vs. the first half and flat during the year. Jobs grew 5.3% in 2022.

Local personal incomes will finish 2023 up 3.2% – up from 0.5% growth in 2022 but half of 6.4% seen in 2021.

And Orange County consumer spending, measured by taxable sales, will continue to moderate – will be up 3% for 2023. But that’s nowhere near the early pandemic spending spree: a 12% jump in 2022 or 23% in 2021.

Orange County housing will suffer an even sharper chill.

House hunters are balking at high prices and lofty mortgage rates. The 23,679 projected home sales for 2023 will be an 11% drop in a year and 22% below the pre-pandemic buying pace of 2018-19.

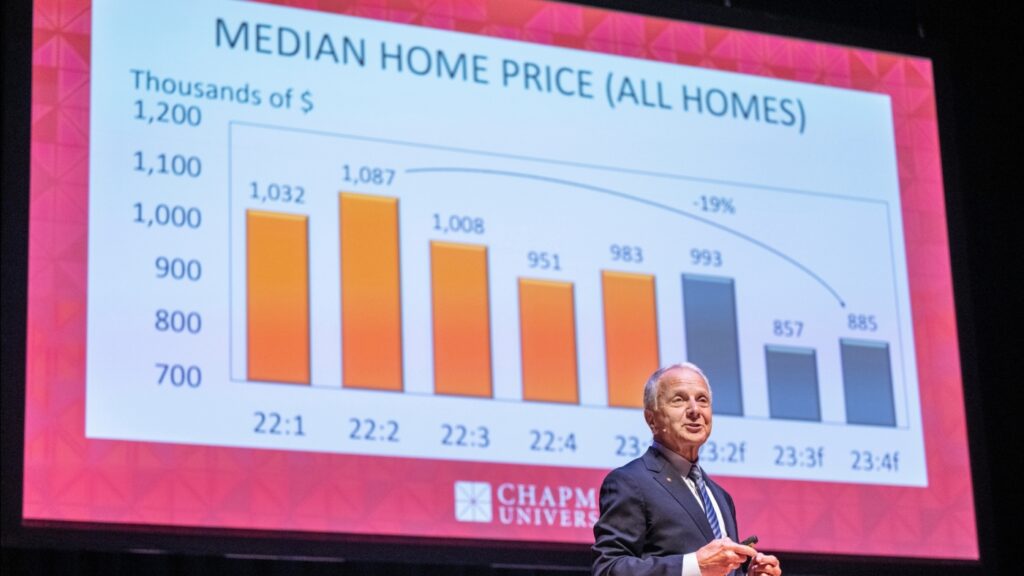

Limited housing demand translates to Chapman’s forecast of a year-end local median sales price of $885,000 – an 11% drop from $993,000 in June and 19% off the $1.1 million high of spring 2022. Chapman predicts an 8% dip for U.S. and California home prices by year’s end, too.

Unaffordability

It’s not that Orange Countians don’t want to own a home, it’s that few house hunters have the financial strength to make a purchase pencil out at current prices.

“The lack of housing affordability is wreaking havoc,” the forecast states.

Mortgage rates that started 2022 averaging 3.8% for 30-year loans now run 6.4%. Chapman sees rates falling to 5.8% by year’s end as the economy slows down.

In an odd way, this year’s costlier mortgages may have prevented larger price losses, Doti says. Homeowners with cheap loans acquired in the mid-pandemic days won’t give up that low-rate financing. So they’re in no rush to sell.

“Prices would have dropped way more if there was any semblance of supply to buy,” Doti said.

The projected cheaper loans, plus the forecasted price cuts, should help more Orange County house hunters qualify for a purchase. But the affordability picture is still not pretty.

Chapman economists estimate that at year’s end, the local median income will be 60% of what’s needed by a successful buyer of the median-priced home vs. 49% in June. But this local affordability yardstick averaged 77% in 2018-19.

The weak sales and pricing will cool homebuilding. The forecast shows permits for single-family houses down 24% in the next six months vs. the first half’s pace. Multi-family permitting will drop 21%.

All of this lethargy will also ice real estate-related hiring, the forecast shows. Orange County construction jobs will slip by 1% in the second half to 103,500. Financial services employment should dip 2% to 110,500.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at [email protected]

Related Articles

House hunter’s nightmare? US home listings fall to record low

California owners lost $59,600 in home equity in a year

Unpopular California: 11% fewer Americans moved to the state over 5 years

How slow is LA-Orange County homebuying? Sales 45% below average

Home sales in Riverside, San Bernardino counties run 29% below average