”Survey says” looks at various rankings and scorecards judging geographic locations while noting these grades are best seen as a mix of artful interpretation and data.

Buzz: California’s growth of its business output ranked just 18th-best among the state during the past three years, more evidence that coronavirus was not terribly kind to the Golden State’s economy.

Source: My trusty spreadsheet reviewed state stats for “real” gross domestic product, a broad measure of business output minus inflation. This measure of economic production is calculated quarterly by the U.S. Bureau of Economic Analysis.

Topline

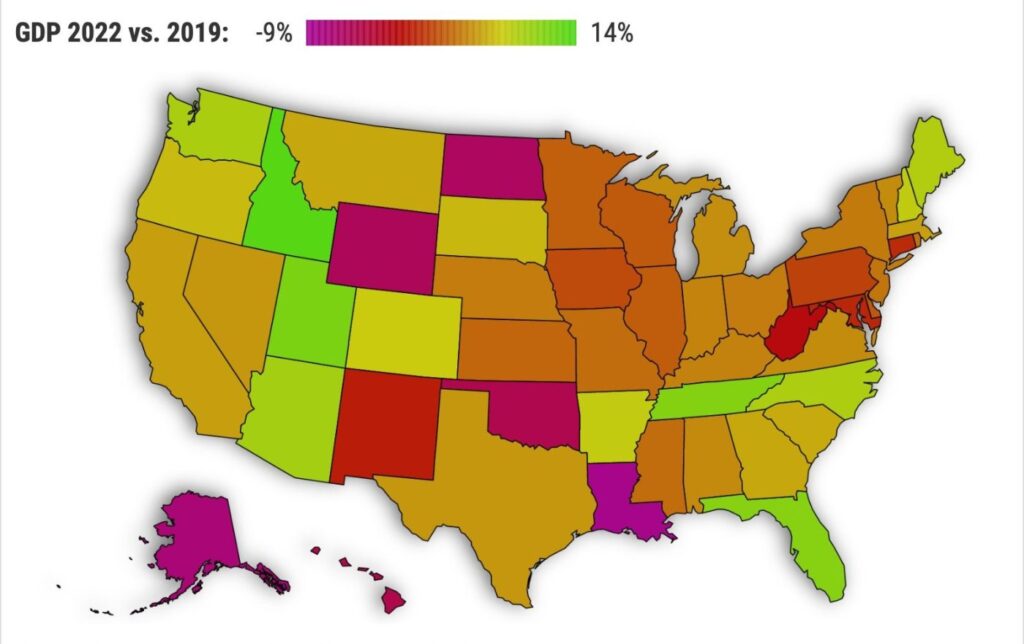

California’s GDP grew 5.7% between 2019 and 2022 – that’s an expansion rate slightly above the nation’s 5.1% growth.

But the increase also trails key economic rivals. No. 1 Idaho saw the value of its business output grow 13.3% in these three years. Then came Utah with 11.6% growth, Tennessee, up 11.1%, Florida, up 10.9%, and Arizona, at 9.5%. Texas was No. 19 at 5.4%.

Worst performances? Louisiana was down 8.4%, then Alaska, off 7.1%, North Dakota, off 5.8%, Wyoming, off 5.5%, and Oklahoma, off 4.9%.

This is a sharp contrast to the business climate of pre-pandemic 2016-19, a time when California GDP growth ranked No. 4 on the state scorecard at 12.4%, well ahead of the 7.7% national pace.

The top states during these three years were Washington, up 16.3%, Utah, up 16.3%, and Idaho, up 13.3%. Texas was No. 10 at 9.9% and Florida was No. 11 at 9.5%.

Worst performances were found in Alaska, off 1.5%, then Mississippi, off 0.3%, Wyoming, up 0.7%, Rhode Island, up 1%, and South Dakota, up 1.2%.

Details

California’s overall economic sluggishness over the past three years wasn’t just pains from 2020’s much-debated efforts to limit the spread of coronavirus. Last year also was a lethargic period for the state’s economy.

For all of 2022, California’s economy ranked 10th worst for GDP growth among the states, advancing only 0.4% vs. a 2.1% national pace.

Top growth was found in Idaho at 4.9%, then Tennessee at 4.3%, Florida at 4%, Nevada at 3.7%, and Texas at 3.4%. Laggards? Alaska, down 2.4%, Louisiana, down 1.8%, Iowa, down 1.5%, North Dakota, down 1.3%, and and Oklahoma, down 1%.

California did finish the year on a modest upswing. Statewide GDP grew at a 2.4% annual rate in the fourth quarter, No. 24 nationally. But the U.S. economy expanded at a 2.6% pace.

Tops were Texas at 7%, then Oregon at 5.6%, Nevada at 5.3%, West Virginia at 5.2%, and New Mexico at 4.8%. Florida was No. 12 at 3.7%. Worst? South Dakota, down 4.3%, Nebraska, down 3.4%, Iowa, down 1.2%, New York, flat, and Connecticut, up 0.1%.

Bottom line

So why was California business output so anemic in a year when the state job market recaptured all the employment lost during the pandemic lockdowns and unemployment hit record lows?

Blame a shortage of workers, a shortfall that came be tied to a host of reasons. One key is the state’s declining population, down 1% between 2019 and 2022. This staffing challenge limits production, boosts wages, and fuels inflation.

Look at interstate flows of people. When my spreadsheet sliced the states into thirds, based on 2019-22’s GDP growth, fast expansion was often found where population was popping.

The 17 top state economies in terms of GDP growth had an average 2.8% population increase over the past three years. The 17 slowest state economies added residents at a 1% average rate.

Also, last year’s end of the Federal Reserve’s cheap money policies – rate hikes designed to cool inflation – was a double-whammy to California.

Low-cost financing is an important fuel for the state’s real estate industries. The end of historically low mortgage rates burst a statewide housing bubble.

Those suddenly higher interest rates also convinced a globe’s worth of investors to seek safer investments. The resulting drops in the stock market were a particularly stiff blow to California’s technology businesses.

Caveat

Let me put the heft of California’s seemingly sleepy economy into some scale.

It remains the nation’s largest in GDP terms, producing $3.6 trillion last year. And that’s 14% of the nation’s $25.5 trillion output. By the way, the next states in production size are Texas at $2.4 trillion, New York at $2 trillion, Florida at $1.4 trillion, and Illinois at $1 trillion.

Consider a global yardstick. The only national economies with more GDP dollars last year, according to the International Monetary Fund, were China ($19.9 trillion), Japan ($4.9 trillion), and Germany ($4.3 trillion). Just behind California were India ($3.5 trillion) and the United Kingdom ($3.4 trillion).

Or ponder that the value of California’s 2022 output was larger than the combined GDP of 24 states (Vermont, Wyoming, Alaska, Montana, South Dakota, Rhode Island, North Dakota, Maine, Delaware, West Virginia, Hawaii, New Hampshire, Idaho, New Mexico, Mississippi, Nebraska, Arkansas, Kansas, Nevada, Iowa, Oklahoma, Utah, Kentucky and Alabama) plus the District of Columbia.

And Californias $11 billion in GDP growth last year, while a minor percentage gain, ranked as the 18th largest advance among the states in total dollars.

Politically speaking

It’s getting close to thinking about the next presidential election, so let’s look at pandemic GDP growth defining “blue” vs. “red” states as those who supported President Biden vs. those who did not.

The 25 blue states, plus D.C., accounted for 62% of the U.S. GDP in 2022. Three-year growth in the pandemic era was 4.7% vs. 7.6% in 2016-19 before the coronavirus upended the world’s economy.

The 25 red states, with 38% of the national economy, grew 5.5% in 2019-2022 vs. a 7% expansion the previous three years.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at [email protected]