The real estate transaction industry seems really antsy about the possibility that home prices might fall — and ignores the “affordability” created by such declines.

Many trackers who saw little chance home prices would dip in 2022 now drop odd hints that they might have been wrong.

Poor forecasting is an occupational hazard for so-called “experts” in any crowd. What’s worrisome is what these gurus are preaching.

Market analysts seem to see no benefit from falling prices, even if it’s one way to create more financially attainable options for house hunters. (Would drivers care if cheaper gasoline hurt the energy industry’s profits?)

So, why are many housing researchers reluctant to say “wait for prices to fall”? Or, you know, there’s a housing “sale” coming?

I fear it’s because prices have become so insane for so long that the hope of a big payoff on a housing “investment” has become the major ownership lure — rather than the comfort such “shelter” brings.

The shot at appreciation drives too many individuals home seekers — not to mention investors who make up 30% or so of all home purchases.

In essence, forecasting no price gains means there’s little else to sell.

Not semantics

I don’t mean to pick on Lawrence Yun, but the chief economist for the National Association of Realtors does influence the industry’s mindset.

He oddly stated earlier this month on LinkedIn that “money invested in the stock market a year ago has quickly dissipated. Money invested in housing may have easily doubled in the past year (e.g., $30,000 down payment on a $300,000 home that rose by 15% to $345,000 would yield a $45,000 gain).”

Then he added: “But future home price gains will not be as strong. There is a possibility of tipping negative if mortgage rates shoot up to 7%.”

What does the stock market’s retreat after a lengthy upswing have to do with buying a house?

Yun previously insisted home prices wouldn’t fall in 2022. He also saw the year’s home sales pace running flat with 2021. Instead, it’s now down 8% through May. And he misread mortgage rates, forecasting a slight rise to 3.7% from 3%. We’re at 5.5% now.

OK, he’s got a cloudy crystal ball. That happens.

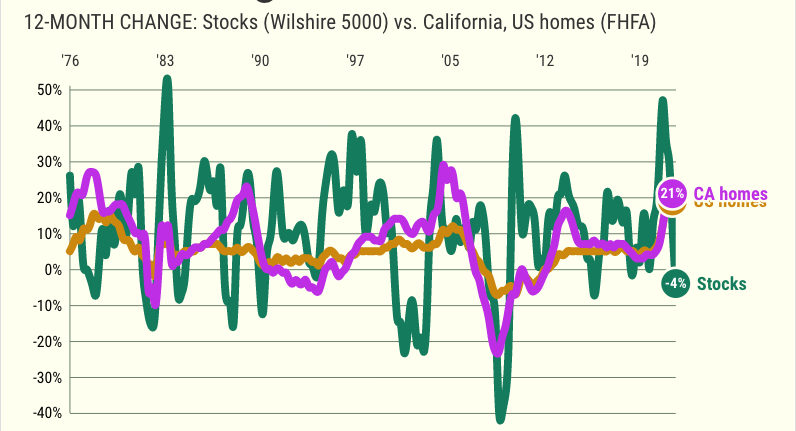

And, yes, the Standard and Poor’s 500 Index, the stock market’s key barometer, declined 21% in 2022’s first half. It was the worst start to a year on Wall Street since 1970.

But talk about “dissipated” hyperbole. At best, horrible word choice.

The Collins online dictionary says “when something dissipates or when you dissipate it, it becomes less or becomes less strong until it disappears or goes away ” or “When someone dissipates money, time, or effort, they waste it in a foolish way.”

This isn’t semantics. Reasonable stock investors know it’s a long-term game. Even after the rough start to 2022 — a much-needed correction, I’ll add — the S&P 500 has grown at an 8% average yearly pace since June 1970. Home prices, by the math from dqydj.com, rose just 5% annually.

Costly investment?

So what about Yun’s homes-vs.-stocks analysis? It features a hypothetical buyer who put $30,000 down a year ago on that $300,000 home that appreciated by 15% in a year — generating a $45,000 “gain.”

Imagine what that home costs to buy, own and sell.

To unload that home and reap that “profit,” let me estimate transaction costs (commissions, fees, etc.) of 6% — that’s roughly $21,000 spent just to unload the investment.

Let’s also assume a 3% rate mortgage from June 2021 — remember those days? — another $8,000 cost. Paying one point for that loan, another $2,700. And let’s generously assume 1% property taxes, another $2,700. Of course, we haven’t mentioned home insurance costs or maybe, association fees.

Related Articles

Midterm forecast: Gas prices get GOP control of U.S. House

Is home-price growth finally cooling?

Prices cut on 12% of homes for sale: What city has the most discounts?

Bubble watch: California economy chilled by Wall Street bear markets

1987: When mortgage rates last soared this much

That’s a lot of cash to amass, even if some expenses are tax-deductible and there’s significant savings vs. paying rent.

Stocking up

Let’s look at stocks like homes — year-over-year results.

Assume the same $30,000 downpayment one year ago was put in Vanguard’s giant index fund — the $1.2 trillion Total Stock Market Index Fund. The investor would get roughly $26,000 back today — a $4,000 loss after a 13% dip the past 12 months.

By the way, the fund owner paid nothing to buy, nothing to sell — and just $12 in management fees. Yes, 0.04%. And owning Vanguard funds — or another other stock investment — required no home upgrades or repairs.

Also, I insist you remember financial leverage — investing when using borrowed money — is a two-edged sword.

Imagine if Yun’s hypothetical “winning” owner stays an owner. Imagine if home prices were to fall 22% from today. (Not that I’m saying they will.)

But if they did, the $30,000 downpayment and the past year’s $45,000 paper profits are gone. And that’s before selling expenses, etc.

Now that’s dissipated.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at jlansner@scng.com