Last October, after nearly 62 years of marriage, Huntington Beach homeowner Patricia Fisher lost her husband. She also lost some of their retirement income with his passing.

Fisher needed to paint her home, repair termite damage and repair cupboards and a shower. She also needed some extra cash.

“The inflation part is huge,” said Fisher. “You never know what can come up.”

The Fishers paid under $200,000 for their home in 1998. Today it’s worth $750,000.

Fisher recently refinanced her mortgage, getting a cash-out, 10-year interest-only loan. Her payment dropped by $158 to $645 a month on a new $200,000 balance. Her interest rate also decreased, dropping to 3.875% rate from 4.25%. She lowered her monthly payment by 20% and walked away with the funds she needed.

Might I remind you just how difficult Fannie and Freddie made it for self-employed borrowers to qualify for home loans because of the imploding COVID-19 economy. Sinking year-to-date income often meant mortgage credit denied.

How much money is in your wallet? How stable is your job or your customer base as recession chatter picks up?

If your answers are not enough cash or not enough stability, perhaps you, too, should consider a cash-out refi. Best to have the money and not need it then need it and not have it.

Some mortgage lenders are getting nervous.

On Tuesday, May 31, Quontic Bank, one of only two fog-the-mirror, no-income documentation lenders, abruptly pulled the plug on its popular no-doc loan for purchases and refinances. If your loan wasn’t already scheduled to close, too bad.

In its memo to mortgage brokers, Quontic cited “safety and soundness considerations,” including their inability to get AAA securitization ratings for such loans and concerns about the unaffordability of house payments as interest rates rise.

“We must ensure that we do not repeat mistakes of the last credit crisis of 2009/10,” the memo said.

Full disclosure: my firm is a longtime Quontic Bank customer.

But it’s not all doom and gloom. On the very same day of Quontic’s announcement, Kroll Bond Rating Agency issued a positive research report about fog-the-mirror CDFIs (Community Development Financial Institutions) and the return of the ‘no-doc’ loan.

If lenders follow prudent guidelines and sound underwriting, the report said, “some lenders may be able to strike a balance between expanding the availability of housing credit … without exposing investors to risks that accompanied pre-global finance crisis no-doc lending.”

Kroll did not respond to my request for comment about Quontic running the other way.

Raymond Sfeir, economic research director at Chapman University, expects fixed-rate mortgages to hit 6.5% by the end of 2022 after the Fed has signaled plans to raise short-term rates by 1.25% to 1.5% by September.

“If that is the case, (home) affordability will sink rapidly,” Sfeir said. “We are forecasting prices in Orange County and California to fall between now and the end of the year. We might have a recession in the second half of 2023.”

Longtime certified appraiser Lance Siegel, president of HVCC Appraisal Ordering Service, predicted home prices will drop from 5-15% in the next two years.

Even though cash-out inquiries are certainly increasing of late, cash-out refinances surprisingly plummeted from the fourth quarter of 2020 to the fourth quarter of 2021, according to Attom Data Solutions. Los Angeles County saw a 77% decrease, Orange County saw a 90% decrease, Riverside County saw a 75% decrease and San Bernardino County saw a 64% decrease.

“The current $27 trillion amount of home equity is the highest ever,” said Rick Sharga, executive vice president of market intelligence at Attom. “(But) if there is concern about jobs not being stable, it’s tough to tap into home equity if you’re not employed.”

Keep in mind cash-out refinances are tax deductible if they’re used for home improvements, according to CPA Marcelo Sroka.

For example, if your current mortgage balance is $600,000 and you pull out an additional $150,000, then the interest paid on all $750,000 is deductible, provided you spend all the cash-out funds on home improvements. Or let’s say $100,000 was used for home improvement and the other $50,000 was used for your kids’ college tuition. You can deduct mortgage interest on $700,000.

“(For) any combination of a new first (mortgage), or a first and second, deductions are capped at $750,000,” said Sroka.

Is Quontic Bank panicking and needlessly cutting off loans in process? Or is it a responsible response to handwriting on the wall?

Either way, loans crumbling ahead of funding will be the new normal in the months ahead. That’s what happens when property values soften, the economy craters and mortgage lenders lose confidence.

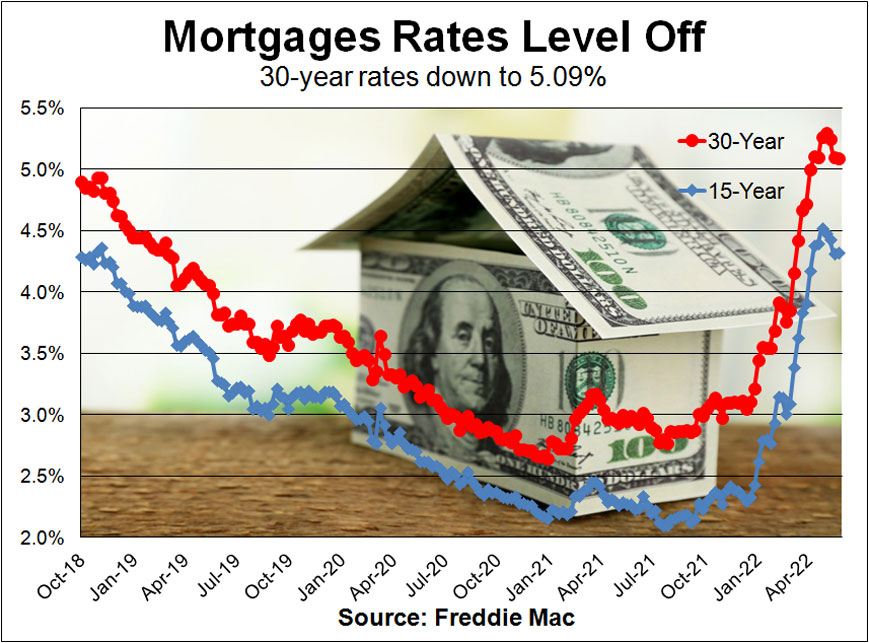

Freddie Mac rate news: The 30-year fixed rate averaged 5.09%, 1 basis point lower than last week. The 15-year fixed rate averaged 4.32%, 1 basis point higher than last week. The 5-year adjustable-rate mortgage averaged 4.04%, 16 basis points lower than last week.

The Mortgage Bankers Association reported a 2.3% decrease in mortgage application volume from the previous week.

Bottom line: Assuming a borrower gets the average 30-year fixed rate on a conforming $647,200 loan, last year’s payment was $785 less than this week’s payment of $3,510.

What I see: Locally, well-qualified borrowers can get the following fixed-rate mortgages without points: A 30-year FHA at 4.5%, a 15-year conventional at 4.25%, a 30-year conventional at 5%, a 15-year conventional high-balance ($647,201 to $970,800) at 4.875%, a 30-year conventional high-balance at 5.375% and a 30-year purchase jumbo at 4.75%.

Eye catcher loan of the week: A 30-year adjustable cash-out jumbo, locked for the first five years at 3.875% with 1 point.

Jeff Lazerson is a mortgage broker. He can be reached at 949-334-2424 or jlazerson@mortgagegrader.com. His website is www.mortgagegrader.com.

Related Articles

Mortgage rates dip as homebuying hints at ‘normalizing’

Mortgage rates are in for a bumpy ride in June

Which president did the best job with inflation?

Unique loan offers no income threshold for underserved homebuyers

Biggest jump ever: Southern California house payments up 37%, topping $3,000 a month