“Numerology” tries to find reality within various measurements of economic and real estate trends.

Buzz: Renting in California, as costly as it is, is a far better deal today than being a homebuyer — an estimated savings of $112,000 over the next five years for the typical tenant vs. the new owners of a mid-priced residence.

Fuzzy math: Numerous reasons exist to own your home — even in today’s rough market. But too many rent-vs.-buy calculations or homebuying affordability metrics don’t represent reality.

Source: My trusty spreadsheet’s review of rents and home ownership costs in 50 big metro areas across the nation from Zillow — including a half-dozen in California — seeking to find the true cost of the roof above one’s head over the next five years.

Top Line

The typical Californian renter in these big six metro areas can expect to pay an average $3,190 a month to the landlord in the next five years — and that cost assumes mid-2022 rents increase at a 4% annual rate.

Meanwhile, a California homebuyer can expect to spend on average $5,054 a month in the same period. This expense includes making house payments on a 5.5% fixed rate no-money-down mortgage; paying property taxes at a 1.5% annual rate; paying down 8% of the mortgage balance; and tax savings worth an assumed 20% of interest and taxes paid.

The result is a $1,863 savings per month for renters — or $112,000 extra paid by owners over five years.

And if this math does not hit home hard enough, so to speak, consider that a hypothetical California buyer in mid-2022 needs 17% appreciation — after 6% closing costs — to sell five years from now and break even vs. renting.

Locally speaking

The state’s six big metros have a wide range of results in this rent-vs.-buy math. Let’s examine the half-dozen by the size of a renter’s expected savings …

San Jose: $3,641 a month spent on rent over five years, No. 1 among the 50 U.S. metros. That compared to an $8,317 monthly net house expense, also No. 1 — for a $1.7 million residence. That’s $4,676-a-month renter savings or $280,500 over five years. So home prices must appreciate 23% over five years to break even.

San Francisco: $3,551 rent, No. 2 nationally, vs. $7,291 on a house, No. 2 — for a $1.5 million residence. That’s $3,739 a month saved by renters or $224,400 over five years. So home prices must appreciate 22% over five years to break even.

Los Angeles-Orange County: $3,229 rent, No. 5 nationally vs. $4,546 on a house, No. 3 — for a $948,000 residence. That’s $1,317 a month saved by renters or $79,000 over five years. So home prices must appreciate 15% over five years to break even.

San Diego: $3,314 rent, No. 4 nationally vs. $4,489 on a house, No. 4 — for a $936,472 residence. That’s $1,175 a month saved by renters or $70,500 over five years. So home prices must appreciate 14% over five years to break even.

Further from the ocean the renter’s edge thins with moves away from densely populated cities.

Sacramento: $2,520 rent, No. 9 nationally vs. $2,945 on a house, No. 8 — for a $623,735 residence. That’s $424 a month saved by renters or $25,500 over five years. So home prices must appreciate 10% over five years to break even.

Inland Empire: $2,887 rent, No. 8 nationally vs. $2,766 on a house, No. 13 — for a $585,904 residence. Yes, renters will pay $121 a month more than buyers, or $7,300 over five years. But if pondering home prices after 6% closing costs, there must be 5% appreciation over five years for the market in Riverside and San Bernardino counties to end up a rent-vs.-buy tie.

Nationally focused

The U.S. math isn’t as kind to renters.

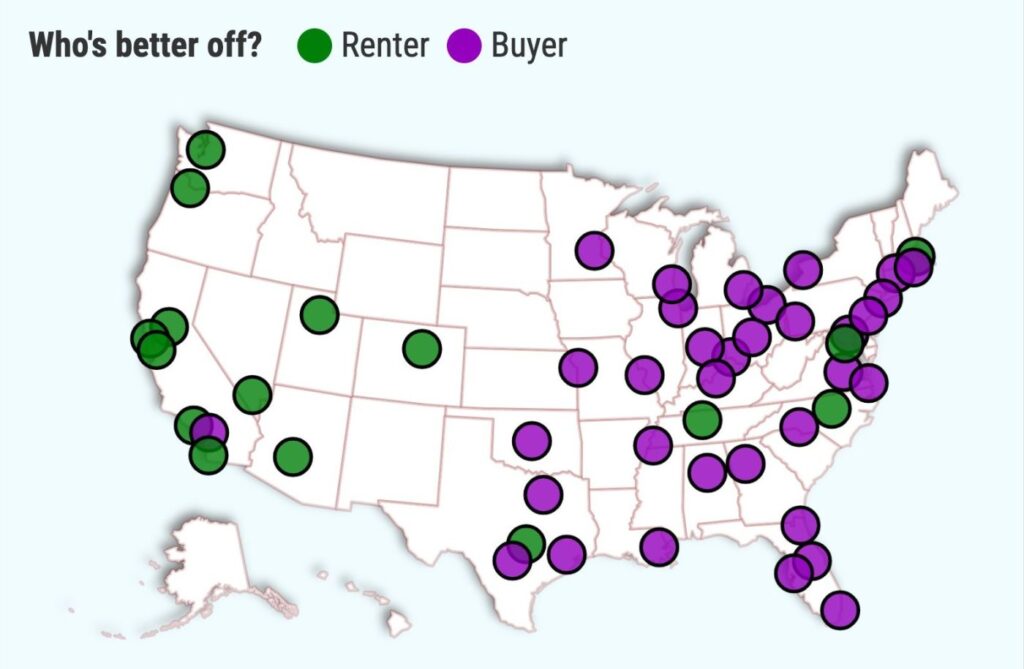

Outside of California, renting is better in only 11 of the 50 metros — Austin, Boston, Denver, Las Vegas, Nashville, Phoenix, Portland, Raleigh, Salt Lake City, Seattle and Washington, D.C.

Nationwide, typical expected rent spending is $2,187 monthly vs. a $1,651 net house payment for a mid-priced $349,816 residence. That’s a $535 a month premium expense for tenants. And that adds up to $32,100 over five years.

So home prices — after closing costs — could decline 4% over five years and renters would just tie their homebuying neighbors, by this math.

Bottom line

My cost analysis isn’t perfect but it helps explain the challenging housing market of mid-2022. Overpriced ownership opportunities help slow the purchasing pace as rents aggressively rise.

Related Articles

1.3 million Californians are late on their rent, Census says

Airbnb permanently bans parties at its rental locations

Apartment rent hikes: Where were Southern California’s biggest jumps in May

Why renters are willing to live in expensive big cities like LA, San Francisco

Yes, everybody’s cost of living differs but you need apples-to-apples measurements to gauge what a seeker of shelter may do. I used “no-home-down” loans for my math. It’s not conventional financing but these deals represent a realistic comparative cost of buying yardstick to rent expenses.

The alternative is to ignore the hefty downpayments required to slash California house payments. Here’s what 20% down would cost around the state — San Jose ($341,000), San Francisco ($300,000), L.A.-Orange County ($190,000), San Diego ($187,000), Sacramento ($125,000) and the Inland Empire ($117,000).

On the other side of the debate, a pair of ownership benefits frequently are ignored by purchase-cost indexes.

The portion of the monthly check to the lender that reduces the loan balance seems rarely discussed. Shrining the mortgage is forced savings by the owners, money they’ll get back when they sell. Over five years that equals roughly 8% of the original mortgage balance at today’s rates. Hey, many landlords won’t even return security deposits.

Plus, mortgage interest and property taxes can be deductible for income tax purposes. Note that no two taxpayers are alike and limits curtail use of these ownership deductions. But there is scant tax aid given to tenants. (Note: The standard deduction for all filers can trim ownership tax savings.)

Yet no matter the formula, mid-2022’s reality strongly favors the renter in California — and landlords know it. That helps explains recent aggressive rent hikes.

Rising rents are a major risk for renters, however, the uncertainty of future housing expenses isn’t part of the typical analysis of homebuying finances either.

Jonathan Lansner is business columnist for the Southern California News Group. He can be reached at jlansner@scng.com